The High Cost of 'Business as Usual': Why Your Credit Card Fees Aren't Set in Stone

Audit your statements → Eliminate junk fees → Reclaim your profit.

Most business owners treat their monthly merchant statement like a utility bill. You glance at the total, sigh at the deduction from your bank account, and move on. You’ve been told for years that these rates are simply "the cost of doing business."

But here is the reality: the credit card processing industry is a lawless frontier. It’s largely unregulated, complex by design, and filled with “stealth leaks” that drain your revenue every single day.

If you think those high rates and fluctuating fees are set in stone, you’re riding into town with your wallet wide open. You’re playing by the processors’ rules.

It’s time to bring in a sheriff-level advocate. You can get leveled up without switching processors, without buying new equipment, and without the headache of retraining your staff on new software.

The Myth of the “Standard” Rate (a.k.a. the Posted Price on the Saloon Door) 💸

When you signed up for your current processor, you likely saw an attractive headline rate, maybe 2.6% or 2.9%. But when you actually do a hidden credit card fees analysis, you’ll find your "effective rate" is significantly higher.

Why? Because the industry is unregulated. While the CARD Act of 2009 protected consumers from certain predatory practices, those protections don’t extend to the merchant side. Processors are free to add markups, invent "service fees," and reclassify transactions into higher-cost tiers at their own discretion.

The "Cost of Doing Business" is a Lie.

High fees aren't an inevitability; they are a choice made by your provider. According to research from Forbes Advisor, typical processing fees range from 1.5% to 3.5%, but the variation within that range is where your profit disappears.

Anatomy of a Transaction: What Are You Actually Paying For? (Follow the Money Trail)

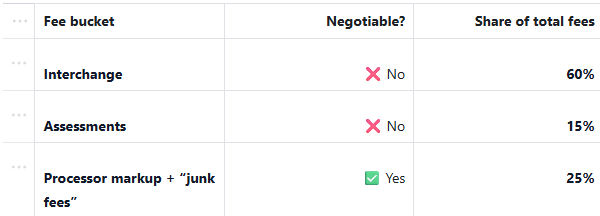

To understand how to save, you have to understand where the money goes. Every transaction is split into three main buckets:

Interchange Fees: Set by the card networks (Visa, Mastercard). This is non-negotiable and goes to the bank that issued the card.

Assessment Fees: Paid directly to the card brands for the use of their network. Also non-negotiable.

Processor Markup: This is the "Wild West." This is where your provider adds their profit, their overhead, and, all too often, their "junk fees."

This third bucket is 100% negotiable.

Quick read (frontier edition): Interchange + assessments are the “toll roads.” Processor markup is the “whatever we can get away with.”

Chart: Where the Average Processing Dollar Goes

What’s negotiable vs. not (frontier rulebook):

❌ Non‑negotiable: Interchange (issuing bank), Assessments (Visa/MC)

✅ Negotiable: Processor markup, Monthly minimums, PCI compliance fees

Should You Switch Processors? Sometimes — But It’s Not the First Lever (Don’t Burn Down the Town) 🚫

The standard advice from most "consultants" is to switch to a new provider. Sometimes that is the right move. But a lot of the time, switching creates a new set of problems—rate creep, new contracts, surprise fees, and a painful integration that burns hours your team doesn’t have.

Here’s the more useful truth: you have options.

In an unregulated industry, high fees aren’t “the cost of doing business”… they’re often just the result of bad pricing and zero accountability.

We believe in a different approach: start with leverage first, then decide if switching is actually worth it. That’s the idea behind Don't Switch—not as a rule, but as a smart first step.

For many businesses, the most efficient way to increase margins is to stay exactly where you are and demand a better deal. When you get leveled up without switching processors, you keep your workflow, your team avoids disruption, and your software integrations stay intact.

But if your current provider won’t play ball—or your setup is fundamentally wrong—we’ll tell you that too. The goal isn’t “never switch.”

The goal is pay less for the same payments… and stop treating hidden fees like a fact of life.

The Statement Protocol: Performing a Hidden Credit Card Fees Analysis (Your Frontier Trail Map) 🔍

How do you know if you’re being overcharged? You need to look for the "Stealth Leaks." These are small, seemingly insignificant charges that add up to thousands of dollars in lost profit annually.

Tiered Pricing Traps: If your statement lists "Qualified," "Mid-Qualified," and "Non-Qualified" transactions, you are likely overpaying. Processors use these categories to hide massive markups.

Ancillary Fees: Look for "Statement Fees," "Reporting Fees," or "Batch Header Fees." These are often pure profit for the processor.

Data Inconsistency: Are you being charged "Card Not Present" rates for transactions that were actually swiped or dipped? This is a common error that drains better margins from your bottom line.

By conducting a professional hidden credit card fees analysis, you can pinpoint exactly where the bloat exists. This isn't just about "saving money": it's about reclaiming revenue that is rightfully yours.

Merchant Advocacy: Your Sheriff in a Lawless Fee Frontier

In a complex, unregulated industry, you need an advocate. Think of it like a specialized legal or tax defense. You wouldn't represent yourself in a complex multi-state tax audit; why would you negotiate with a multi-billion dollar processing conglomerate on your own?

At Clear Harbor Group, we act as that advocate. We use our industry knowledge and proprietary data to negotiate pricing with your provider—or, when it makes sense, help you evaluate alternative setups that reduce your total cost.

Here’s why this matters: the “processor markup” bucket is where most of the games are played. And because the industry is largely unregulated on the merchant side, many businesses are paying inflated pricing simply because nobody is challenging it.

This is how our clients get leveled up without switching processors. We don’t force a rip-and-replace. We focus on outcomes—lower effective rates, fewer junk fees, and pricing you can actually defend.

And for businesses that want to go even further… there’s a modern option that can help you take back your profits at the point of sale.

Dual Pricing: A Powerful Way to Take Back Your Profits (Put Up Clear Prices in Town) 💰

If your goal isn’t just “lower fees,” but stop letting processing costs quietly eat your margin, dual pricing is worth a serious look.

Dual pricing displays one price for card payments and a lower price for cash/ACH—so the cost of card acceptance is reflected in the card price instead of silently deducted from your profit on the back end. This means you can take back control of your margins on every transaction.

Here’s what that changes:

Your pricing becomes intentional—not dictated by a processor’s markup.

Your margins stop bleeding on high-ticket invoices.

Your customers get clarity at the point of sale (clean signage, clear receipts, no confusion).

Dual pricing isn’t right for every business or every state/use case. But when it’s implemented correctly—with compliant setup and clear customer communication—it’s one of the most direct ways to take back your profits instead of just hoping your fees behave.

Description: A simple before/after graph comparing “Effective Rate (Before)” vs. “Effective Rate (After Advocacy),” illustrating reduced processor markup while interchange stays steady.

What This Is vs. What This Is NOT

It’s important to clarify what this strategy looks like in practice, because there is a lot of noise in the merchant services world.

What This IS:

Expert Negotiation: We use our leverage to force your processor to lower their markup.

Zero Downtime: Your terminals, software, and daily routines stay exactly the same.

Ongoing Monitoring: We don't just lower the rate once; we watch your statements every month to ensure the processor doesn't try to sneak those fees back in.

Risk-Free: Most advocacy models are contingency-based. If we don't find savings, you don't pay.

What This IS NOT:

A forced switch: Staying with your current provider is often the cleanest path—but it’s not the only option.

An Equipment Sales Pitch: We aren't here to sell you a fancy new iPad stand or a wireless terminal.

A Temporary "Introductory" Rate: These are permanent structural changes to your merchant agreement.

The Bigger Picture: Total Profit Reclamation 🚀

Saving $500 or $1,000 a month on processing fees might not seem like a "blockbuster" move on its own. But when you combine it with other strategies: like plugging the silent revenue leak at your front desk or utilizing an 80-lender financing network to increase case acceptance: the cumulative effect is massive.

We call this the Total Profit Reclamation Strategy. It’s about looking at every area where your practice or business is losing money to "the system" and taking it back.

Stop Accepting the Status Quo

If you are running a high-volume medical practice, a dental office, or a professional service firm, those "small" processing fees are likely costing you tens of thousands of dollars every year. In an unregulated industry, silence is interpreted as consent. If you don't challenge your fees, your processor will continue to increase them.

You’ve worked too hard to build your business to let it be a piggy bank for a merchant service provider. It’s time to stop paying the "cost of doing business" and start keeping more of what you earn.

Educational • No-pressure • Obligation-free

Ready to see what’s actually hiding in your statements?

Gather your last 3 months of processing statements.

Request a hidden credit card fees analysis.

Review the findings and see what options you have to lower your effective rate.

Sources: